Benefits

The History of Retirement Benefits

By Liz Davidson

Jun. 21, 2016

Our retirement is not our parents’ retirement. For many American employees in their generation, a good job meant access to a secure retirement income they could not outlive. Employers took center stage, assuming most of the financial risk of funding that retirement with employees largely removed from the process. Today, employers are far more likely to be facilitators of retirement saving, playing a critical supporting role while the employee is the star planner of the retirement show.

How did the idea that employers should offer secure retirement benefits through defined benefit plans, or pensions, evolve? How and why did this change over time to put more of the responsibility on employees to save through defined contribution plans such as 401(k)s? And how can benefits managers use new savings tools and employee benefits available today to help their employees retire smarter, happier and more financially secure?

The U.S. Retirement System

Retirement is a fairly modern concept with origins in military history. Until the late 1800s, those who had to work to earn their living worked their entire lives. Historians credit the Roman Empire with conceiving the idea of an income that continued after work service by offering pensions to retiring soldiers during the first century B.C. While this initiated a long tradition of military pensions, the concept of ceasing to work in later life didn’t begin to spread to the rest of the workforce until the 19th century.

Today, we think of a pension as a series of payments to be made to workers after the end of their working years. In the United States during the mid-1800s, a “pension” also referred to disability and survivor benefits. During the middle of that century, larger cities began to offer disability and retirement income benefits to police and firefighters. This trend expanded over time among public sector workers.

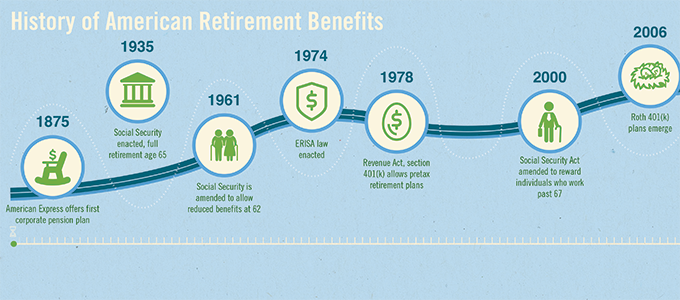

In 1875, The American Express Co. created the first private pension plan in the U.S. for the elderly and workers with disabilities. According to the Pension Research Council, by 1926 approximately 200 private pensions had been established by larger employers in the United States. Early pension benefits were designed to pay out a relatively low percentage of the employee’s pay at retirement and were not designed to replace the employee’s full final income.

The idea that employees should have some kind of a defined benefit in retirement gained traction during the boom decades that followed World War II. Large corporate employers took a paternal approach to their workers and offered pensions as part of their talent recruitment and retention efforts.

And it worked. It was not uncommon for workers to spend their entire careers at the same company back then. Compare that to 2014 when the U.S. Bureau of Labor Statistics reported the average employee tenure was 4.6 years.

Benefits grew richer over time, with many pension plans offering replacement incomes that covered more of the employees’ average pay. By 1970, 26.3 million private sector workers (45 percent of all private sector employees) were covered by some kind of pension plan. Participation held steady for several decades with 43 percent of private sector employees still covered by 1990.

With a traditional defined benefit plan, employees had little direct control over their retirement. To earn higher lifetime benefits in the plan, they could work longer, make a higher salary or live longer — but the employer controlled the contribution formula and the investments, and generally made all the contributions to fund the plan.

The ’70s brought America staggering inflation, disco, and legislation that changed retirement forever. In 1978, Congress passed The Revenue Act of 1978 in which Section 401(k) cleared the way for the establishment of defined contribution plans. The idea was revolutionary: Employees would be able to contribute their own money in a tax-advantaged way to an account to supplement any other retirement benefits they had with tax incentives for the employer to also contribute. The upshot? Over the past 38 years for the typical U.S. employee, the responsibility for developing a sustainable retirement income has shifted from the employer to the individual.

A “defined contribution plan” takes its name from the ability of the employee and/or employer to contribute a fixed sum to the plan. Over time, different types of plans evolved to serve different types of employees: 401(k) plans for private sector employees, 403(b) plans for nonprofit and public education employees, 457 plans for state and municipal employees and the Thrift Savings Plan for federal employees.

Today, the traditional pension is an endangered species. For the past decade, employers have been terminating defined benefit plans in record numbers and moving toward defined contribution plans. According to the Employee Benefits Research Institute, by 2011 69 percent of employee participants in a retirement plan at work were participating in a defined contribution plan, 24 percent were participating in both a defined contribution and a defined benefit plan, and just 7 percent were in a defined benefit plan only.

Employees are Unprepared or Underprepared for Retirement

Employees are largely unprepared to shoulder the risk of saving adequately to fund retirement and making wise investment choices with those savings. According to the Financial Finesse 2015 Year in Review research on employee financial trends, only 22 percent of employees are confident that they are on track for retirement, even though 84 percent contribute to their retirement plan. (Editor’s note: The author is the CEO of Financial Finesse.)

When it comes to choosing appropriate investments in their retirement accounts, employees are also falling short. Only 46 percent of male employees and 36 percent of female employees are confident their investments are allocated appropriately in their retirement accounts. Problems with cash flow management and debt have a cascading effect on suppressing retirement savings rates.

Recent enhancements in retirement plan design, such as auto-enrollment and auto-escalation, are not enough to increase preparation. Employers must address cash management and overall financial wellness, educating them to better understand their role in retirement preparation and freeing up more funds for contributions toward their retirement goals. Integrating plan design enhancements with employee benefits education and communication can improve retirement preparedness.

Employers can increase the likelihood that employees will be better prepared for retirement by integrating retirement education into an overall financial wellness program that looks at cash flow, employee benefits and long-term financial goals. When in place, Financial Finesse’s research shows repeat users of workplace financial wellness benefits have shown a 88 percent improvement in the percentage of workers who are on track for retirement. Forward-thinking employers can take these six steps to improve employee retirement preparedness:

- Increase the default deferral rate.

- Automatically enroll employees in auto-escalation of their retirement savings.

- Implement re-enrollment in the plan’s qualified default investment alternative, also known as a QDIA, an investment that may be used by retirement plan sponsors in the absence of direction from the plan participant.

- Offer benefits planning to help employers understand and maximize the value of their benefits.

- Enhance employee communications.

- Develop a comprehensive financial wellness program.

More — and More Complex Benefits Choices

Employers and employees are also navigating major changes in health insurance benefits, including the move to high deductible health plans in conjunction with health savings accounts, which were created in 2003. Employees in general do not yet fully understand the advantages of HSAs in preparing for retirement, and employers have a high hurdle in helping them maximize this benefit.

Additionally, since the Roth individual retirement account was introduced in legislation sponsored by the late-Sen. William Roth Jr., R-Delaware, in 1997, Americans within certain income limits have been able to save after-tax contributions in an account that grows tax-free for retirement. The Roth 401(k), allowed by legislation passed in 2001, gave those employers who sponsor retirement plans the option to offer employees after-tax/tax-free distributions within the 401(k) structure. While slow to gain adoption, recently employees have been choosing Roth options in greater numbers.

Healthy Confusion

Employees generally remain confused over which health insurance and retirement plan options are best for their situation. They look to their employers to offer guidance on how to choose what’s right for them. Employers may consider offering targeted educational workshops or webcasts, print or email communications and personal financial coaching to help employees understand and maximize these benefits.

For health care, this includes ways to review the health coverage and out-of-pocket costs they have today, understand and compare plan options, decide which option is best for their unique situation and prepare for changes they’ll need to make in their cash management to take full advantage of the value of an HSA. Employers can also offer workers retirement plan education on the differences between pretax and after-tax contributions, and the general types of situations where one or the other makes sense.

The good news is that employers are well-positioned to help employees be the star planner of the retirement show so they can meet the challenges of improving retirement preparedness and make wise benefits decisions. According to a TIAA survey, 81 percent of respondents said they trust financial information from their employer. Financial Finesse’s 2015 Retirement Preparedness Research shows that the number of employees who say they are on track for retirement doubled with repeat usage of workplace financial wellness programs. While technology such as online financial education can play a supporting role, employers will gain the most influence and employee satisfaction with offering interaction with a financial coach who can help employees through the decision-making process.

Employers who offer support, guidance and education to assist employees in taking center stage throughout their careers in order to retire comfortably will have loyal, more financially confident employees. As reporter Emily Brandon said in “Pensionless: The 10-Step Solution for a Stress Free Retirement,” “Although you may never receive a pension from a former employer, you can do a lot to make the most of the retirement benefits you do have.”

With employers leading the way in prepping workers for the future, 21st century employees can still have a comfortable, secure retirement.

Schedule, engage, and pay your staff in one system with Workforce.com.